GST is the single indirect tax that is levied on the supply of goods and services between different entities. GST returns are the tax return forms that are required to be filed by these entities with the Income Tax authorities of India. This is used by tax authorities to calculate tax liability.

As per GST rule, any business whose annual turnover is more than the prescribed limit shall get a GST Identification Number, which is a 15-digit alpha-numeric, PAN-Based and State Specific unique number.

Input tax credits paid at each stage will be made available in the following stage of value addition. GST is basically a tax levied on value addition at each stage. Therefore, the consumer has to pay only the GST charged by the last dealer or supplier in the supply chain.

This can be done by filing online returns. GST Returns are the Goods and Services Tax Return forms that taxpayers of all types have to file with the income tax authorities of India under the new GST rules.

Individual taxpayers will be using 4 forms for filing their returns such as:

Different Types of Returns applicable under the new GST Law

| Return form | Who should file the return and what should be filed? |

|---|---|

| GSTR-1 | Registered taxable supplier should file details of outward supplies of taxable goods and services as effected. |

| GSTR-2 | Registered taxable recipient should file details of inward supplies of taxable goods and services claiming input tax credit. |

| GSTR-3 | Registered taxable person should file monthly return on the basis of finalization of details of outward supplies and inward supplies plus the payment of amount of tax. |

| GSTR-4 | Composition supplier should file quarterly return. |

| GSTR-5 | Return for non-resident taxable person. |

| GSTR-6 | Return for input service distributor. |

| GSTR-7 | Return for authorities carrying out tax deduction at source. |

| GSTR-8 | E-commerce operator or tax collector should file details of supplies effected and the amount of tax collected. |

| GSTR-9 | Registered taxable person should file annual return. |

| GSTR-10 | Taxable person whose registration has been cancelled or surrendered should file final return. |

| GSTR-11 | Person having UIN claiming refund should file details of inward supplies |

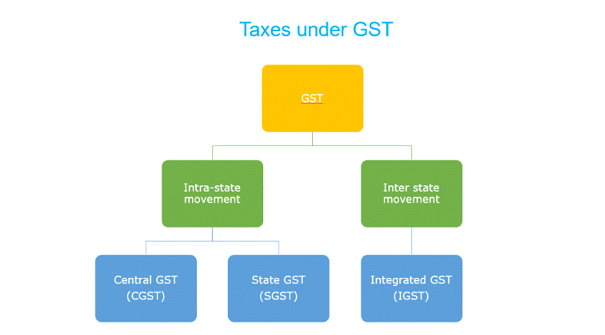

To determine whether Central Goods & Services Tax (CGST), State Goods & Services Tax (SGST) or Integrated Goods & Services Tax (IGST) will be applicable in a taxable transaction, it is important to first know if the transaction is an Intra State or an Inter-State supply.

Under erstwhile taxation laws, Central Government levied taxes on, manufacture of certain goods in the form of Central Excise duty, provision of certain services in the form of service tax, inter-State sale of goods in the form of Central Sales tax.

Similarly, the State Governments levied taxes on retail sales in the form of value added tax, entry of goods in the State in the form of entry tax, luxury tax and purchase tax, etc.

So any tax which were levied by the Central Government or the State Governments on the supply of goods or services has now been converged in goods and services tax, which is a dual levy where the Central Government will levy and collect tax in the form of central goods and services tax (CGST Act 2017) and the State Government will levy and collect tax in the form of state goods and services tax (SGST Act 2017) on intra-State supply of goods or services or both.

This implies that both the Central and the State governments will agree on combining their levies with an appropriate proportion for revenue sharing between them. However, it is clearly mentioned in Section 8 of the GST Act that the taxes be levied on all Intra-State supplies of goods and/or services but the rate of tax shall not be exceeding 14%, each.

The features of Central Goods and Services Tax Act, 2017, are as follows:

A simple understanding could be that, when SGST is being introduced, the present state taxes of State Sales Tax, VAT, Luxury Tax, Entertainment tax (unless it is levied by the local bodies), Taxes on lottery, betting and gambling, Entry tax not in lieu of Octroi, State Cesses and Surcharges in so far as they relate to supply of goods and services etc. are subsumed into one tax in GST called State GST. All the tax proceeds collected under the head SGST is for State Government.

The scope of IGST Model gives meaning to the GST Act of which IGST is one of the components. The IGST Act clarifies that Centre would levy IGST which would be CGST plus SGST on all inter-State transactions of taxable goods and services with appropriate provision for consignment or stock transfer of goods and services.

The seller making supply outside the state will pay IGST on value addition after adjusting available credit of IGST, CGST, and SGST on his purchases. And the exporting State will transfer to the Centre the credit of SGST used in payment of IGST.

On the other hand, the Importing dealer will claim credit of IGST while discharging his output tax liability in his own State. The Centre will then transfer to the importing State the credit of IGST used in payment of SGST.

The relevant information will also be submitted to the Central Agency which will act as a clearing house mechanism, verify the claims and inform the respective governments to transfer the funds.

All goods and services transacted in India under GST are classified under the HSN code system or SAC Code system. Where services are classified under SAC Code and goods are classified under HSN Code.

HSN or HS (Harmonised Commodity Description and Coding System) is a multipurpose international product nomenclature developed by the World Customs Organization (WCO).

HSN standardizes the classification of merchandise under sections, chapters, headings, and subheadings. This results in a six-digit code for a commodity (two digits each representing the chapter, heading and sub heading.

Under GST, the majority of dealers will need to adopt two-, four-, or eight-digit HSN codes for their commodities, depending on their turnover the year prior.

HSN codes are introduced for classifying goods for taxation. It's all designed to bring about more uniform taxation as well as more ease of doing business. HSN codes will now be used in filing returns, on invoices, etc., rather than written descriptions

Services Accounting Code also called as SAC Code is a classification system for services developed by the Service Tax Department of India. Using GST SAC code, the GST rates for services are fixed in five slabs namely 0%, 5%, 12%, 18% and 28%.

Note: If a service is not exempted from GST or if the GST rates are not provided, then the default GST rate for services of 18% would be applicable.